Casual observers could be forgiven for thinking the collapse of the cryptocurrency exchange FTX is another typical tale of financial mismanagement. That’s how its founder, Sam Bankman-Fried, terms it: a liquidity crisis that tipped over into a solvency one.

FTX had deposits and loans and when depositors tried to get their money back, FTX didn’t have it to hand. Sure, the loans were in fancy digital money, rather than stale dollars, but at first glance, it appears like just another big company failure.

Then you look closer, and it becomes clear that the whole edifice is in fact the corporate equivalent of three children in a trenchcoat pretending to be a fully grown man.

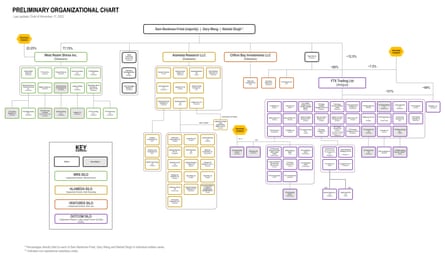

It is a story that encompasses a financial black hole inside a company once valued at $32bn (£27bn), a byzantine group structure with unclear lines of ownership, and a leadership with a highly unconventional approach to governance and interpersonal relations.

That chaos was laid out in excoriating terms in a bankruptcy filing submitted on Thursday by John Ray III, who replaced Bankman-Fried as FTX’s chief executive after its collapse on 11 November. “Never in my career have I seen such a complete failure of corporate controls and such a complete absence of trustworthy financial information as occurred here,” he wrote. Bear in mind this is the man parachuted in to oversee the collapse of energy company Enron after its fraud was revealed.

“From compromised systems integrity and faulty regulatory oversight abroad, to the concentration of control in the hands of a very small group of inexperienced, unsophisticated and potentially compromised individuals, this situation is unprecedented,” Ray added.

The company, he said, did not have a simple liquidity crisis, or even a simple insolvency one. On Wednesday, Bankman-Fried claimed the “semi-liquid” assets of FTX.com were still worth $5.5bn, a significant chunk of the outstanding $8bn it owes depositors. Ray gave a different valuation for those assets: $659,000. All of FTX’s holdings combined, including $1bn of “stablecoins” and $483m of cash, were in fact worth less than $2.5bn.

But FTX.com is only part of the business. The wider group is formed of a sprawling network of more than 100 related companies, all shared through the common ownership of Bankman-Fried and two of his co-founders, Gary Wang and Nishad Singh. No single investor other than the co-founders owns more than 2% of the equity of any of the four main “silos” that make up the group: FTX’s US crypto exchange, its hedge fund Alameda, its venture capital arm, and its international exchange.

Ray’s filing details every way you could imagine a multibillion-dollar company run by a trio of inexperienced hedge fund graduates could go wrong, and then some.

The Alameda silo had $4bn of loans made to “related parties”, including $2bn to Bankman-Fried’s personal company, Paper Bird, and a further $1bn to Bankman-Fried himself. The international exchange owed money to its depositors, but did not track that in its own financial statements. The group as a whole “did not maintain centralised control of its cash”, did not have an accurate list of bank accounts, and did not pay attention to the creditworthiness of banking partners.

It gets worse. No one was able to put together a list of FTX staff, Ray said. He had “substantial concerns” about the financial statements assembled under Bankman-Fried, and said they should not be treated as reliable. The group was used to buy homes for employees; the digital assets were controlled through “an unsecured group email account”.

“Unacceptable management practices include … the use of software to conceal the misuse of customer funds,” the filing added. “Very substantial transfers” of property may have occurred in the “days, weeks and months prior” to the bankruptcy, it continued, while on the day of bankruptcy, “at least $372m of unauthorised transfers” occurred.

On Friday, those last unauthorised transfers were revealed to have been made at the behest of the Bahamian government, which claimed it was taking the money for “safekeeping”, and launched a legal battle to try to wrest control of the bankruptcy case from the US. In a response from FTX (pdf), the company accused the Nassau government of having flouted the freeze on FTX assets that was put in place specifically to ensure funds were not waylaid, and implied that the country was working with Bankman-Fried, who is “effectively in the custody of Bahamas authorities”, to undermine the bankruptcy case.

Ray’s report ended with a final, personal, note. “Mr Bankman-Fried, currently in the Bahamas, continues to make erratic and misleading public statements. Mr Bankman-Fried, whose connections and financial holdings in the Bahamas remain unclear to me, recently stated to a reporter on Twitter: ‘F*** regulators they make everything worse’ and suggested the next step for him was to ‘win a jurisdictional battle vs Delaware.’”

The document makes for astonishing reading, but barely scratches the surface of FTX. Take its fourth major player, Caroline Ellison. Bankman-Fried’s sometime girlfriend, the 28-year-old was head of trading at Alameda before being promoted to jointly run the hedge fund in summer 2021, and was left in sole charge this year when her counterpart Sam Trabucco abruptly quit to spend more time with his boat.

If Bankman-Fried was the public face of FTX on Twitter, Ellison was its Tumblr equivalent. In posts on her account, since deleted, she wrote about her understanding of traditional finance (“it’s very unlikely for you to actually lose all your money”), her ideal man (“controlling most major world governments [and having] sufficient strength to physically overpower you”), and her exploration of polyamory. “When I first started my first foray into poly, I thought of it as a radical break from my trad past,” she wrote in 2020, “but tbh, I’ve come to decide the only acceptable style of poly is best characterised as something like ‘imperial Chinese harem’. None of this non-hierarchical bullshit. Everyone should have a ranking of their partners, people should know where they fall on the ranking, and there should be vicious power struggles for the ranks.”

It’s hard to know where to stop. Ellison, Bankman-Fried, and eight others in the group’s inner circle shared a luxury penthouse in the Bahamas, according to a report in Coindesk that saw the inner circle dubbed a “polycule” by, among others, Elon Musk.(That penthouse has now been put up for sale for $40m.) According to one report, an in-house psychiatrist was on hand to dole out prescription stimulants; photos of Bankman-Fried at his desk appear to show an empty box of one such medication.

In the days leading up to the collapse of the company, Wang, its co-founder, continued to code, making changes to a private repository hosted on coding platform GitHub. Wang has not been available to answer questions about what the urgent programming job was.

In the days following, Bankman-Fried took to Twitter to try to defend his reputation, which he did in part by tweeting the word “what” and the letters “H A P P E N E D” in nine separate posts over 36 hours. At the same time, he was sending direct messages to Kelsey Piper, a journalist at Vox, giving a rather different side of the story.

Some of those direct messages include the “fuck regulators” line quoted by Ray in the filing. Others contain the clearest explanation yet of what did happen – the trigger that toppled the years-long pile of mismanagement.

FTX didn’t have a bank account that customers could send money to; Alameda, the hedge fund, did. So they would wire the cash to Alameda, and FTX would add it to its account. And, in all those years, Alameda never passed the cash on. No one noticed, and the firm apparently traded, and lost, $8bn of customer funds that it should never have had in the first place.

“Each individual decision seemed fine and I didn’t realise how big their sum was until the end,” Bankman-Fried told Piper. “Sometimes life creeps up on you.”