Thanks in large part to the rise of streetwear — and the elevation of the sneaker into a status symbol — alongside the impact of the pandemic on lifestyles, designer footwear shoppers today are looking for both comfort and statement styles that push the boundaries of traditional features. The latest report from BoF Insights, The New Statement Shoe: Reimagining Designer Footwear, explores this creative shift and what it means for brands jostling for market share in this multi-billion-dollar category.

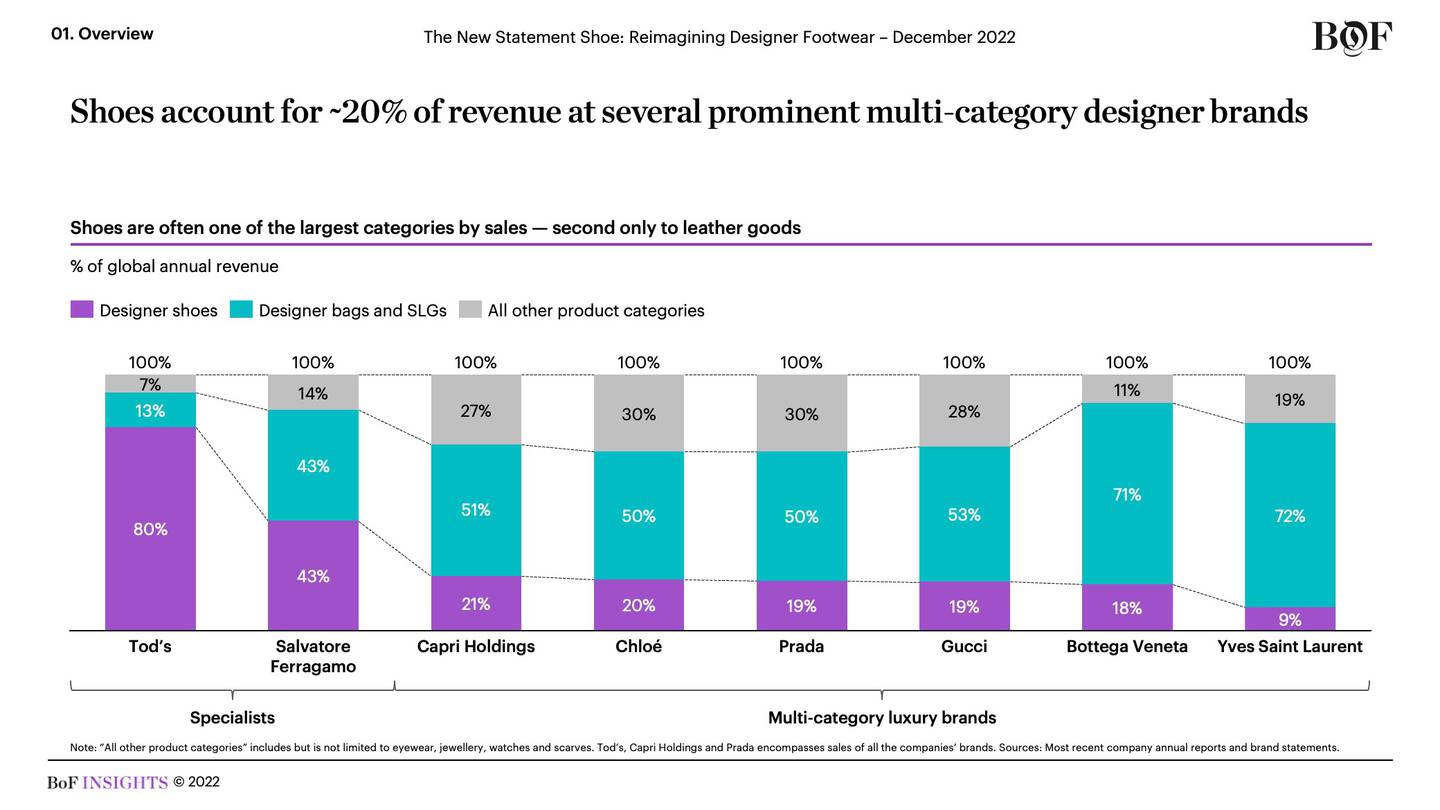

According to market research firm Euromonitor International, designer shoes are expected to grow globally from $31 billion today to $40 billion by 2027. Designer shoes are a “power category,” meaning they function as highly visible opportunities for fashion brands to display house codes like logos on the vamp or signature stitching, while satisfying consumer desires for experimentation and self-expression. Shoes can also be important revenue drivers, accounting for between 10 percent and 25 percent of overall sales for some of the most prominent multi-category luxury brands.

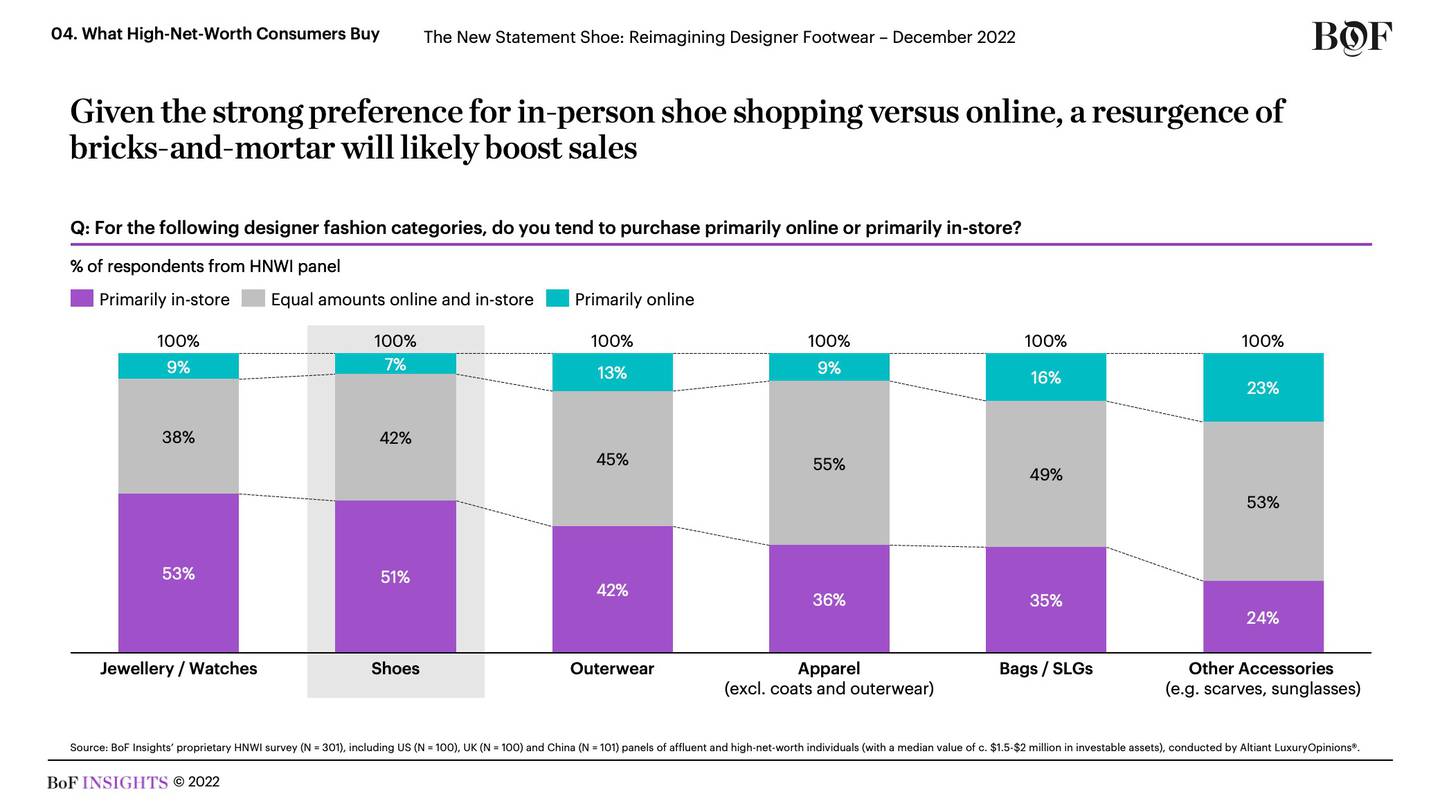

Designer shoes stand to benefit from a post-pandemic shift in fashion consumer behaviour, including the return of in-person shopping. BoF Insights fielded a survey via Altiant, a luxury and wealth research firm, of 300 high-net-worth individuals in the US, China and the UK — each with investable assets worth a median value of around $1.5 million to $2 million. All surveyed HNWIs were “engaged” in the category, defined as having either purchased designer shoes in the last year and / or intending to purchase designer shoes in the next year. The survey found that 51 percent purchase designer shoes primarily in-store, compared to 36 percent who purchase apparel primarily in-store.

Additionally, HNWIs have changed what they are looking for when shopping for designer footwear since the onset of the pandemic – 72 percent of the surveyed HNWIs say they tend to look for more comfortable shoes now, while 63 percent say they are more likely to seek versatility in their designer shoes to reflect a lifestyle shift. Moreover, over half of the surveyed HNWIs say they are seeking out more statement shoes than before the pandemic.

This desire for a combination of style and comfort underpins the growing popularity of designer variations and collaborations with comfort-oriented shoe brands, such as Birkenstock teaming up with the likes of Dior and Manolo Blahnik.

But there is still room for heels, as in-person events and special occasions return to post-pandemic levels. Data provided for the BoF Insights report by fashion search engine Tagwalk reveals that 16.4 percent of the shoe styles on runways during SS2 were high heels, compared to only 8.5 percent in SS22.

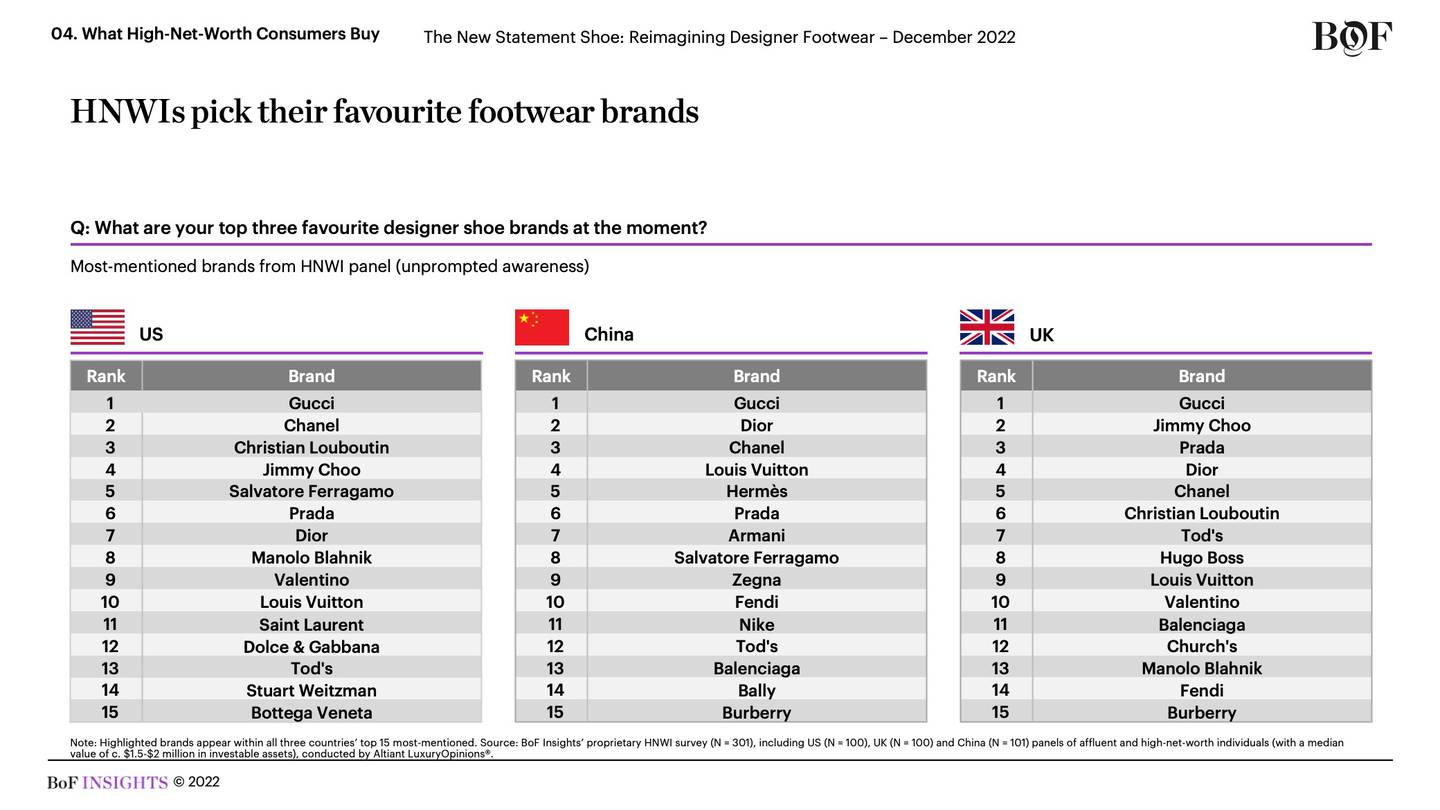

BoF Insights’ survey also reveals which brands are resonating the most with HNWIs. Gucci leads as a brand favourite, with Chanel, Dior, Prada and Louis Vuitton consistently appearing in the top 10.

Against this backdrop, the competitive landscape indexes on a matrix of price versus fashion-forwardness, with innovation across features including silhouette, heel height, heel shape, materials, colour and sole innovation. Novelty is introduced season after season with the potential to become a brand emblem or patentable feature, which can translate well on social media and generate viral success. For brands, this means the power of a statement pair of shoes is greater than ever.

As part of a series of category-focused analyses from the team at BoF Insights — The Business of Fashion’s research and data unit — the latest report explores how brands and retailers must rethink growth strategies in the face of designer footwear shoppers’ evolving preferences and motivations.

Why this BoF Insights report is a must-have:

- Analyses the global market for designer shoes (products defined as having a minimum retail price of $300)

- Features proprietary research with high-net-worth consumers in the US, UK and China, revealing the most in-demand brands and styles, budget by demographic group, drivers of purchase decisions and intent to spend on particular styles

- Provides executive perspectives on the breadth of assortment, pricing strategy, creative development and collaborations between brands

- Presents concise case studies on Amina Muaddi, Balenciaga, Birkenstock, Gucci, Loewe and Salvatore Ferragamo while exploring the complexity behind designing and manufacturing shoes in terms of SKUs and variations, plus the power of specialisation

- Unpacks how the forces of casualisation and the acceleration of comfort-dressing are widening the definition of luxury for designer shoes and assesses how the consumer psyche post-pandemic has shifted towards more statement shoes

This report is based on four proprietary research inputs:

- Three panels conducted by Altiant LuxuryOpinions® on behalf of BoF Insights of HNWIs in the US, UK and China who each have investable assets with a median value of between $1.5 million and $2 million

- 20 interviews with founders, CEOs and other senior executives from designer shoe brands, retailers, and consultants

- Market sizing data from Euromonitor International, a global market research firm

- Tracking of shoe styles and categories on the runway from 2019 to 2022 in New York, Milan, Paris and London, enabled by data from Tagwalk, a fashion runway search engine

- An analysis of US in-stock options, styles and average unit prices of designer brands, enabled by data from Edited, a retail intelligence and AI-driven data insights company

- In-person store audits and pulse interviews conducted at designer shoe brands and luxury retailers in the US and UK

- Featured companies include but not limited to: Amina Muaddi, Balenciaga, Birkenstock, Chanel, Christian Louboutin, Dior, Gucci, Jimmy Choo, Loewe, Mach & Mach, Manolo Blahnik, Nike, Prada, Stuart Weitzman, Tod’s, Valentino and and Versace