For many fashion businesses, addressing climate-related risks is often a priority that is eclipsed by other challenges they deem more urgent or imminent. However, due to the geographic footprint and structure of fashion’s supply chains, it is especially vulnerable to extreme and increasing climate volatility. In 2024, a mindset shift is needed across the industry to acknowledge that maintaining the status quo is no longer an option and climate risk cannot be viewed as a long-term project to be tackled further down the line. The past year has provided ample examples of why climate de-risking needs immediate action given fashion value chains’ exposure to extreme weather conditions around the world. De-risking will not be the sole responsibility of manufacturers — brands will also need to revisit their supplier standards and invest to ensure they are sufficiently addressing new climate-related dimensions.

Globally, 2023 will likely be remembered as a year of climate-related disasters, and the frequency of these disasters is only expected to increase due to climate change. Soaring temperatures around the world will make 2023 one of — if not the — hottest years on record, which scientists say is the result of both El Niño weather patterns and global warming. Sweltering temperatures, wildfires, torrential rain and flash floods have devastated communities around the world, leaving behind death and destruction. Few regions seemed to be spared.

Though the human and environmental tragedy looms large, it is also hard to ignore the economic toll. The US, for example, had suffered an annual record, at $23 billion, of climate-related disasters even before 2023 comes to an end, surpassing 2020′s record high. And drought in Argentina in 2023 could cause the country’s economy to shrink by 2.5 percent, according to the International Monetary Fund. Beyond the Americas, China lost more than $7.6 billion due to severe drought in 2022. Globally, the cost of each climate-related disaster is estimated to have increased 77 percent over the past 50 years, reports the World Economic Forum.

As global warming exceeds its current level of 1.1°C above pre-industrial levels, productivity growth is set to fall. With global warming levels potentially reaching 2.2°C by 2050, global GDP levels could be reduced by up to 20 percent, while warming of up to 5°C by 2100 could lead to “economic annihilation,” according to Oxford Economics.

The BoF-McKinsey State of Fashion 2024 Executive Survey found that executives expect other challenges — notably economic uncertainty, geopolitical tensions and inflation — to be vying for their attention ahead of climate risk. Yet, the past year should be a wakeup call for fashion. With fashion still responsible for between 3 percent and 8 percent of total greenhouse gas emissions, a mix of short- and long-term strategies can help companies address the climate challenge. Companies, for example, may look to de-risking the value chain and revamping structural and operational legacies, or doubling down on sustainability.

Outsized Risks for Fashion’s Value Chain

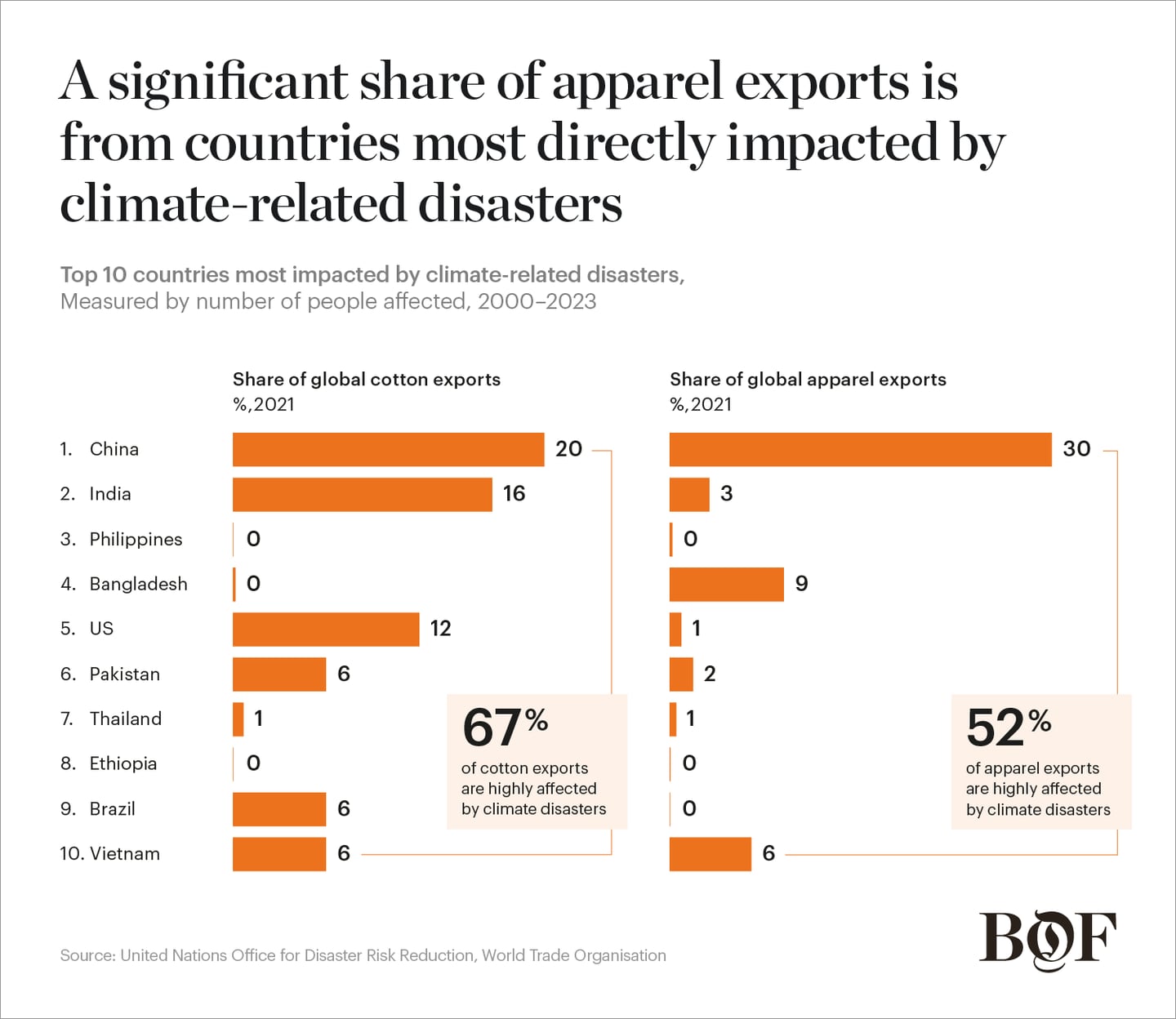

Every part of the fashion value chain is affected by the climate crisis, not least because so much of the industry is reliant on the countries and regions most directly impacted by climate upheavals, signifying an outsized risk for fashion in comparison to many other industries. By 2030, extreme weather events could jeopardise $65 billion worth of apparel exports and eliminate nearly one million jobs in four economies that are among the most central to the global fashion industry — in Bangladesh, Cambodia, Pakistan and Vietnam.

One part of the fashion value chain that is particularly exposed is the production of raw materials supplying manufacturers. Consider cotton, which is sensitive to both droughts and flooding. In India, the world’s second-largest cotton exporter, extensive rainfall and pest invasions have reduced its supply to the extent that the country began importing it. Pakistan, too, has been hit by extreme monsoons, while in contrast, drought has hit Texas’ cotton producers, leading to abandoned crops and steep production declines.

For manufacturers, flooding is also a growing risk, forcing temporary or permanent factory closures. In Ho Chi Minh City, Vietnam, 55 percent of apparel and footwear manufacturing sites could be exposed to rising sea levels and flooding by 2030. Not only are the livelihoods of factory workers impacted, but their health and safety as well. Factory workers in Dhaka, Bangladesh, report suffering headaches, exhaustion from dehydration and lack of sleep due to high temperatures, while 53 percent of surveyed Cambodian workers reported becoming unwell due to heat stress. Meanwhile, as temperatures climb, productivity is expected to fall significantly, estimated to decrease at about 1.5 percent for every degree that temperatures rise above 25°C.

Climate is also impacting fashion’s logistic strategies. Across all industries, 90 percent of exported goods are reliant on shipping to reach their final destinations, but an estimated $122 billion of economic activity at ports is at risk from disruptions caused by extreme climate events. The summer of 2023 saw Europe’s worst dry spell in 500 years, with ships navigating the Rhine River forced to reduce the weight of cargo in order to continue their journeys. A similar narrative played out on the Panama Canal. In China, drought slowed traffic on the Yangtze River, forcing companies to move goods through alternative, often more expensive routes.

Weather-Proofing Strategies in 2024 and Beyond

Fashion executives in 2024 and beyond should embed climate strategies across their businesses. They may do so by first identifying direct value at risk from potential climate impacts as well as material second- and third-order impacts — such as supply chain disruptions, damage to infrastructure, or financial and job losses — and implementing thorough scenario planning for these possibilities.

Boosting resilience up and down the value chain, particularly in climate risk “hotspots,” is critical. Nimble processes are needed to swiftly offset weather-related pressures on suppliers and inventories as well as consumers. Alongside these operational changes, other adjustments must be considered, including sourcing strategies and locations to ensure they also enable flexibility and speed in times of extreme weather events. This may require trade-offs between risk mitigation and cost, speed, capacity and availability of materials.

Action by manufacturers must take the form of prioritising worker health and safety. This can be actioned through operational shifts such as offering more frequent breaks, rehydration amenities and proactive temperature monitoring of the factory floor, alongside capital investments in fan systems.

Longer term, and most importantly, companies should invest in innovation across the value chain aimed at helping to reduce fashion’s impact on the planet. This will touch on all areas of the value chain, from new material innovations such as lab-grown fibres, more efficient and ethical product reuse and recycling, and a shift from encouraging make-take-waste consumption culture.

Industry-wide initiatives will be crucial to facilitate progress at scale. Joining pacts such as the Fashion Pact, the Sustainable Apparel Coalition and the Fashion Charter is a strong first step, but action must follow alignment. Individual company adaptation should be supported by urgent collaborative change.

This article first appeared in The State of Fashion 2024, an in-depth report on the global fashion industry, co-published by BoF and McKinsey & Company.