Imagine a luxury beachside destination teeming with scantily clad tourists and adrenaline junkies where VIP shoppers mingle with celebrities at events like the local film festival. The setting may sound like a well-known corner of the Mediterranean coast of Europe, but it is, in fact, the idea for a mega-resort being built in a once secretive, insular kingdom in the heart of the Middle East.

The Red Sea Destination on Saudi Arabia’s west coast is just one of the many ‘giga-projects’ currently underway as part of the country’s historic transformation. A manager of Saudi-based developer Red Sea Global has confirmed to Hotelier Middle East that women will be allowed to wear bikinis and mix with men at the luxury resort project set to welcome visitors later this year.

That the dress code became headline news underscores just how wide the gap still is between the kingdom and most Western countries in terms of gender equality and expressions of modesty. But only a few years ago, it would have been unfathomable for such a resort to exist in a country known to be one of the most conservative in the world. Changes are being introduced at a pace that feels fast for most locals, even if it seems slow for some Westerners.

“Saudi Arabia’s transformation cannot be underestimated. It’s impossible to describe just how fast the country is going through, not just economic, but also social change,” said Myf Bagnold, Riyadh-based chief marketing officer at Cenomi Retail (formerly the Alhokair Fashion Retail unit of Fawaz Abdulaziz Alhokair Co.), a Saudi group with a diverse portfolio including partnerships with more than 95 lifestyle and fashion brands such as Zara and Estée Lauder.

Though critics contend that some of the reforms impacting sectors like fashion, hospitality, sports and entertainment are about whitewashing the country’s image and distracting from its poor human rights record, the changes must be seen through both a local and global lens. Whatever one’s perspective, they point to even more opportunities for global brands.

Building New Cities and Neighbourhoods

From Valentino choosing Jeddah as the starting point for rolling out its new global retail concept to Richard Mille’s now annualised Desert Polo Tournament and Dolce & Gabbana’s 2022 Alta Moda and Alta Sartoria show at Al-Ula, an oasis town along the ancient incense trade route, the once closed-off country has become a focal point for luxury industry events and investment in recent years.

While most fashion and beauty brands already have a sizable footprint across malls in both Riyadh and Jeddah, industry leaders believe that further expansion is inevitable. New retail space in mega-developments under construction will play a part, as will a wider roll-out across existing second and third-tier Saudi cities.

“We need to capture the Saudi market today, more than ever, and we need to do it faster. There is an expectation from our partners, from global fashion brands, which is significantly more than what we are currently realising,” said Patrick Chalhoub, group president of Chalhoub Group, a partner for brands including Louis Vuitton and Christian Dior across GCC countries (Gulf Cooperation Council members Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Oman and Qatar).

Last year Saudi Arabia was one the world’s fastest-growing major economies, benefitting from high global energy prices, labour market reforms, and improvements to the business environment. Vision 2030, the transformation blueprint unveiled by crown prince Mohammed bin Salman Al Saud in 2016 with the goal of diversifying and modernising the oil-based economy, is opening up the Gulf’s largest market for investment.

Fifteen colossal ‘giga-projects’, spanning every region of the expansive state, are designed to re-position Saudi Arabia as a global powerhouse in the coming years. Highlights include Neom, the $500 billion futuristic ‘linear city’ stretching across 170 kilometres which will be home to 1 to 2 million square metres of retail space, Diriyah Gate, a 1 million square metre tourism destination designed to highlight Saudi Arabia’s cultural heritage and Riyadh’s new financial hub, King Abdullah Financial District which is in the final stages of completion.

“Vision 2030 is driving a phenomenal change across the kingdom and the retail sector in particular is at the forefront of global interest,” said Faisal Durrani, head of Middle East research at real estate brokerage Knight Frank. Though much of the growth in the property sector will be residential or hospitality, a report by the firm confirms that over 4.5 million square metres of new retail space can be expected in the kingdom by 2030.

Improving Local Retail to Boost Tourism

While growth prospects are robust across much of the GCC region, companies like Chalhoub are prioritising Saudi Arabia mainly because it is still underpenetrated and underserved. This helps explain why locals continue to disproportionately shop abroad, compared to UAE nationals, despite the partial repatriation of luxury spend trend that took place across the region during the pandemic.

“Two-thirds of luxury fashion purchases [by Saudis] are made outside of Saudi Arabia. We should be looking to double, if not triple business there,” Chalhoub said.

The retail value of the Saudi fashion market (apparel, footwear and personal accessories) is currently $24.2 billion whereas the UAE comes in at $22.9 billion, according to data from Euromonitor International. Together, the two countries account for around 50 percent of sales in the Arabic-speaking subregion of the wider Middle East and North Africa (MENA) region, according to analysis in a BoF Insights report.

One reason the UAE fashion market is slightly larger than that of Saudi Arabia — despite the latter country having three times more people and a much larger economy — is that the UAE benefits from extensive retail spending by international tourists. Industry insiders don’t expect any Saudi city to overtake Dubai, either as the regional fashion capital or primary shopping hub, at least in their lifetime, but even modest gains made by Saudi Arabia to attract more tourists to its ancient and modern attractions will help narrow the gap.

This is borne out by Euromonitor International projections showing that the Saudi fashion market will be growing at a faster rate (23.7 percent) than the UAE’s (22.9 percent) in the period between 2023 to 2027. Longer-term, Saudi’s larger and more localised youth demographic will give it an edge.

At the high end of the fashion spending spectrum, Saudi Arabia accounts for around 23 percent of the entire GCC region, making it the second largest luxury market after the UAE, according to Federica Levato, senior partner at Bain & Company. In 2022, the Saudi personal luxury goods market was valued at €2 billion ($2.1 billion), having grown by 9 percent CAGR during the interim pandemic years.

But it is Saudi Arabia’s swelling customer base that makes it a focal point for luxury brands looking to up their investments. Euromonitor’s latest data reveals that the kingdom is expected to see a surge in affluent individuals (with a net wealth of $1 to $5 million) and HNWIs (with a net wealth of above $5 to $50 million) between 2022 and 2030, with the figures increasing from 117,400 and 12,500, respectively to 203,300 and 22,100.

The challenge for some brands looking to capture the market, however, is that they lack a sufficiently nuanced understanding of the local customer.

Distinctive and Diverse Consumer Behaviour

Marriam Mossalli, founder and chief executive of Saudi-based luxury communications agency Niche Arabia said, “Saudi Arabia has its own unique shopping behaviour which is very different from what is seen in neighbouring markets such as Dubai or Kuwait.”

“Saudis tend to be very brand loyal, so acquiring new clients for a brand tends to be more challenging in this market than in others [in the Gulf],” she continued. “If our mother bought into a brand, we will too. Whereas the luxury consumer in Dubai is very trend-driven, whilst in Kuwait, they tend to be a lot more experimental.”

The relative youth and affluence of the Saudi luxury consumer makes them exceptionally attune to the differences in shopping experiences offered locally and globally.

“What brands need to know is that they are coming into a very competitive [retail] landscape,” emphasised Mossalli. “These girls [local luxury consumers] are online 24/7, scrolling, browsing and shopping constantly. They are customers of Net-a-Porter, Matchesfashion and Farfetch, with the majority of them being on VIP or private client level across many of these platforms.”

Aside from its demographic profile, another factor that makes the Saudi market stand out is its sheer scale, with different regions, provinces and cities being home to their own sub-cultures and traditions. Understanding these geographical nuances can be critical to commercial success.

“Riyadh, as a city, is comparable to New York in terms of lifestyle [and people there] tend to be more formal, more dressed up because it’s the banking and governmental capital of the kingdom. Jeddah is like Los Angeles, it’s more laid-back and relaxed, and the shopping preferences there are reflective of that,” Mossalli added.

Both cities should be seen as a part of any market entry strategy, suggests Fahed Ghanim, chief executive officer at Majid Al Futtaim Lifestyle, the fashion retail division of Dubai-based Majid Al Futtaim, a leading regional lifestyle conglomerate with a portfolio comprising of 29 shopping malls across the MENA region and the developer behind Riyadh’s forthcoming $4.3 billion mega shopping mall project, Mall of Saudi.

“We see stronger sales coming out of Riyadh…but Jeddah holds a similar importance. You cannot be in one city, and not the other,” said Ghanim who oversees the operations of brands such as All Saints, Hollister and Lululemon as well as homegrown multi-brand retailer That Concept Store across the Gulf region.

Secondary markets like the coastal city of Dammam, a major administrative centre for the Saudi oil industry in the Eastern province, as well as its satellite city Al Khobar, have seen an uptick in retail investment from luxury brands such as Chopard and Breitling.

Other cities are growing in importance as mass market retail destinations, such as Mecca and Medina, which attract millions of Muslim pilgrims from around the world throughout the year. The pilgrim retail opportunity reflects the changing behaviour of people on hajj or umrah who either diversify or extend their trips to include leisure activities and tourist attractions.

Tertiary markets are also on the up. Al-Ula, a go-to regional holiday destination for royals, influencers and celebrities alike, is becoming a retail centre for companies such as Harvey Nichols, Azza Fahmy and Michael Cinco that have this year launched pop-ups there.

With ongoing developments across every major city including Tabuk, Taif and Jubail, retail investment opportunities for brands are seemingly endless. But this feeling can leave some business leaders coming to the kingdom unprepared.

Lifestyle Shifts in a Rapidly Changing Society

“A lot of brands think that when they come to a market like Saudi or the GCC, you are going to make money from year one. No, you have to earn it. Customers here are sophisticated. The local customers are very well-travelled, you cannot underestimate them,” said Fahed.

Bagnold believes that “the speed of change is definitely one of the biggest challenges. Everything is moving so fast, that knowing what’s coming next, or when it will be implemented, is something that everyone in the country is working to keep up with.”

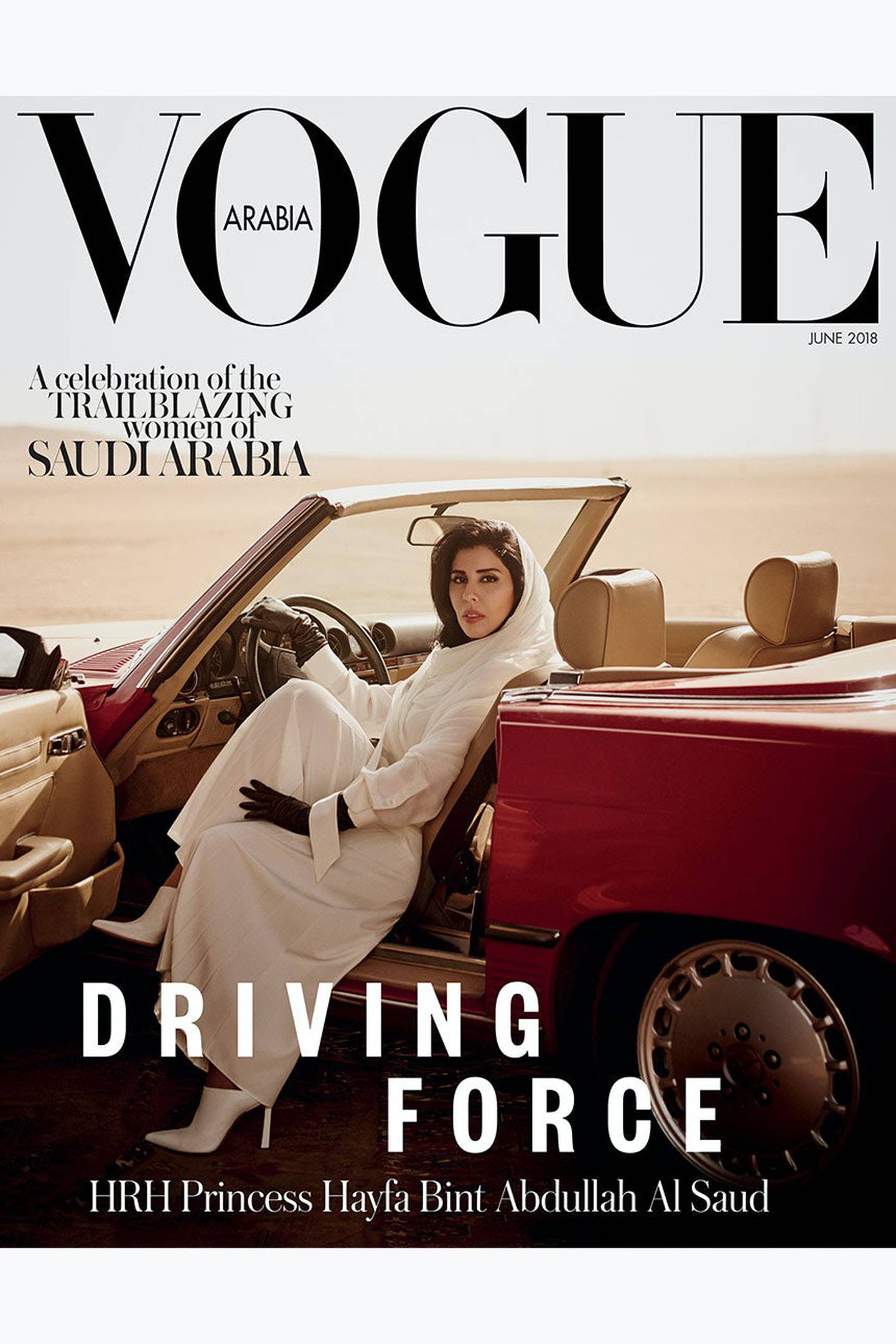

Some of the social reforms introduced by the government in recent years have led to a more balanced society where women are able to commute, work, live, travel and socialise more freely than they were in the past. The introduction of allowing women to drive, as well as the lift on the mandatory abaya and hijab requirements, and the relaxation on male guardianship laws, are among them.

“The changing role of women in Saudi Arabia is a hugely positive movement for the country,” commented Myf Bagnold. “But how we as a retail business cater to it and build upon that, with the right relationships and right offering is definitely a challenge.”

Recent shifts have led to noticeable changes in both female spending power and consumer behaviour.

“What we are seeing now is that, because the woman is entering the workforce, she is more active in her lifestyle, so her requirements as a buyer are changing,” said Mossalli. “She’s buying ready-to-wear over occasion or eveningwear. She is looking for a more contemporary approach to fashion, opting for everyday luxury items that she can wear to work and post on social media.”

Despite significant strides being made on the women’s rights front, the country continues to draw criticism from international human rights groups for codifying its male guardianship system instead of abolishing it. The lack of LGBTQ rights and the severe penalties imposed on homosexuality, which include imprisonment and capital punishment, are also realities that global brands find difficult to navigate.

Although similar penal codes can be found in many countries around the world, including other Muslim-majority states, Saudi Arabia’s position as a G20 country and a key regional market continues to place it under direct international scrutiny.

Balancing Local, Regional and Global Marketing

Given the ever-evolving operating environment, how can brands effectively harness the full potential of the Saudi market amid changes in law, society and culture?

“Keeping up with the regulatory framework is quite challenging. Unfortunately, you cannot take what you have applied in other markets, even Dubai, for granted and use it as a blanket policy. You need to differentiate and localise your approach…It’s a complex market but also a highly rewarding one once you have the right setup in place for it,” Ghanim said.

Other industry leader stress the importance of having stakeholders with local on-the-ground expertise. In the short term, many brands will therefore continue to partner with established retail groups based in Saudi Arabia or the wider Gulf region, such as Saudi Jawahir, Rubaiyat, Chalhoub Group, Cenomi Retail, Al Tayer Group and Majid Al Futtaim.

“One of the mistakes is that brands assume that localised means regionalised. Of course, you cannot [always] treat…every [single] city differently, but Saudi is 35 million people, they have their own tone of voice,” said Patrick Chalhoub, referring to the pan-GCC approach that brands once employed across the Gulf region.

Yet there are instances where the regional approach can be just as effective, or more so, than a dedicated local one. Celebrity and influencer marketing is one example. While some social media stars from Saudi have become well-known on Instagram and TikTok in recent years — Amy Roko, Rawan Abdullah Abu Zeid (also known as Model Roz), Hala Abdallah, Alanoud Badr and Yara Al Namlah among them — regionally famous names from other countries like Lebanon are popular in the kingdom too.

At the same time, fashion brands have started tapping local talent for localised campaigns. When Dior launched its Or collection in alignment with Ramadan this year it oversaw the roll-out of a global capsule collection and ensured that a popular Saudi actress, Aseel Omran, had been appointed ambassador alongside Lebanon’s Razane Jammal for the region.

Other recent collaborations include Mytheresa’s Ramadan partnership with Nojoud Al-Rumaihi, and Alanoud Badr’s (also known as ‘Fozaza’) collaborative capsule with Steve Madden. Using Saudi National Day as a peg, American label Carolina Herrera partnered with local artist Aida Alharthy to develop an exclusive bag that celebrated the traditional Saudi art of al sadu, whilst French jewellery brand Messika launched a limited-edition green and white rendition of a necklace to commemorate the occasion.

However, local industry leaders like Mossalli warn of the pitfalls of brands going too far or falling into the trap of ‘culture-washing’ when trying to cater to the Saudi luxury consumer.

“A lot of times brands come to the Middle East thinking they need to revise their offering, but what they don’t understand is that Saudi women have two different spheres for dressing: public and private. In private she wants to be wearing whatever is being worn on in New York, London or Paris. [So] having an exclusive product or offering for the region is always a good idea, but it really needs to align with the brand’s original DNA for it to make sense to the Saudi consumer.”

Mossalli cites Saudi pride as the reason that many women continue to wear abayas even though they are no longer mandatory. “The younger generation is growing up unapologetically nationalistic, they wear the abaya, not because they are repressed, but because it is an integral part of our cultural identity.”

National pride is also driving support for local designers. The Saudi Fashion Commission, an initiative launched by the Ministry of Culture in 2020 to support the development of the local fashion industry, is heavily invested in nurturing homegrown talent.

One of the highest profile among them is Saudi couturier Mohammed Ashi, founder of Ashi Studio. A red carpet favourite among international celebrities, royals and other high-profile clients, he was the first couturier from the Gulf region to be invited to show on the official Paris couture week calendar this year by the Fédération de la Haute Couture.

“Mohammed Ashi is a leader of Saudi fashion and his creative force has made an invaluable contribution to Saudi’s fashion zeitgeist as the country undergoes a cultural transformation,” said Burak Cakmak, chief executive officer of the commission.

Emerging Saudi designer labels such as Abadia, Nora Al Shaikh, Chador and Noura Sulaiman, are also seeing an uptick in popularity. Meanwhile, regional designers from other Middle Eastern countries are beginning to compete with selected global brands for consumer wallet share in the market thanks to entrepreneurs like Tamara Abukhadra, founder of Jeddah-based multi-brand store Homegrown Market.

Vying for Supremacy as the GCC Hub

Another Vision 2030 initiative, The Regional Headquarters Attraction Programme of Multinational Companies, requiring foreign firms to set up regional headquarters in Saudi Arabia by the end of 2023 to be able to work with governmental entities, is driving investment across multiple sectors of industry. But how it will impact luxury remains to be seen as only a limited number of brands — Piaget, Richard Mille and Van Cleef & Arpels among them —have announced opening dedicated offices in the kingdom.

Even if there is a dash later this year for more brands to open an official headquarters there, industry insiders suggest that brands’ Dubai offices will probably remain their unofficial regional hub. Riyadh, the commercial nerve centre of the kingdom, will become a centre for operations but instead of eclipsing Dubai, it will more likely serve as a complementary hub, with a unique identity and position of its own.

“If we look at the wider Middle East, we currently only have one global hub city, and that’s Dubai,” said Durrani, suggesting that Riyadh is on its way to global city status.

“[But] if you look at other regions of the world, you tend to have multiple global hub cities that are in close proximity to each other. London and Paris, New York and Toronto [etc] – they are all within an hour’s flying time of each other, and they also tend to be the number one destination for each other for passenger traffic by air. Riyadh and Dubai have that pairing in place already.”

Another multi-nodal precedent exists in Asia where there is a growing trend for multinational companies to set up self-contained operations for the giant of that region, China, in a mainland city like Shanghai or Beijing, alongside a pan-Asia regional headquarters in Hong Kong or Singapore.

“Saudi as an economy is one of the world’s twenty largest, so they have their own domestic drivers to feed any industry that grows up there,” continued Durrani. “The UAE, on the other hand, is quite reliant on expats and tourists, so they are quite different from one another. I don’t necessarily see it as one replacing the other, I see them being complementary.”

Navigating New and Old Retail Challenges

Industry leaders suggest that rapid shifts in Saudi’s social and business regulations have led to a customer experience in the physical retail sector that has not always kept pace with international standards.

“The brick-and-mortar retail environment, which is still 80 to 90 percent of the market [in Saudi Arabia] has not transformed yet in comparison to other sectors,” said Patrick Chalhoub. “It’s a work in progress.”

Until recent reforms, the country required fashion retail stores to offer segregated shopping experiences for men and women. Many of these stores have yet to adapt their internal customer journey to meet the level of service that the country’s affluent clients experience in popular travel shopping destinations such as London, Paris or Dubai.

On the regulatory front, the introduction of new laws and updated rules across industry present yet another set of challenges that retailers and brands need to constantly navigate.

Recent updates to the Saudi Nationalisation Scheme, also known as “Saudisation”, have led to the total of 72 professions in the nation being reserved exclusively for Saudi nationals, including fashion retail. Another directive, issued in 2021, stipulates that only Saudis can work in “closed commercial complexes (malls)” and their management offices.

Although in firm favour of the initiative, Chalhoub, along with some of his peers, is concerned about the pace of implementation and extent of expected changes. Compliance continues to be challenging, given the relative youth of the modern retail industry in Saudi.

“To me, the directive of 100 percent Saudisation on the retail front sends a very clear and positive message,” said Chalhoub. “But 100 percent too quickly is not serving Saudi retail talent. You need to have experienced people present on the shop floor to methodically coach, train, supervise and manage junior team members so that they are able to deliver the outstanding service that is expected from luxury brands.”

Despite the challenges around this and other initiatives, localisation is key to success in both the short and long term, he suggests. “We cannot come from London, Paris or even Dubai to Saudi and adopt the same formula in Saudi anymore. We need local expertise to really capture the market.”

“Saudi society is evolving, and because of the youth of the population, it is an ongoing change that has yet to stabilise. The Saudi Arabia of today is not the one of yesterday, but not yet the one of tomorrow,” he added.